You Are Already Non-Compliant (Probably)

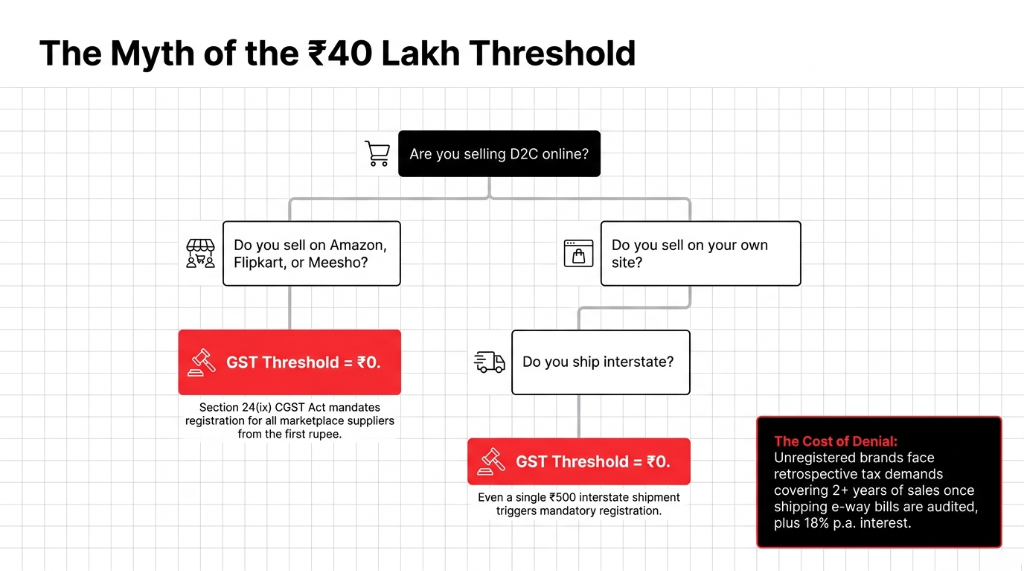

Here is the uncomfortable truth most D2C founders in India do not want to hear: the moment you list your product on Amazon, Flipkart, or Meesho, the ₹40 lakh GST registration threshold no longer applies to you.

Section 24(ix) of the CGST Act, 2017 mandates registration for every supplier on an e-commerce operator's platform. No exceptions. No turnover floor. That founder selling ₹8 lakh worth of skincare on Meesho and thinking they are "below the limit"? Wrong. Open to penalty from the first rupee.

It gets worse when you add your own D2C website. If you are making interstate sales directly — even a single ₹500 order shipped from Surat to Bengaluru — GST registration is mandatory regardless of turnover. We have seen brands making ₹25 lakh/year on Shopify who avoided registration, only to face retrospective demands covering 2+ years of sales once GST authorities flagged their shipping partner's e-way bill trail. Plus 18% p.a. interest.

And if you opened a second warehouse in Maharashtra to reduce shipping costs? Congratulations. You now need a separate GSTIN for Maharashtra — on top of your home state registration. Multiple warehouse locations = multiple state registrations = multiple GSTR-1 and GSTR-3B filings every single month.

The Registration Trap We See Constantly:

Marketplace sellers: GST threshold is ₹0. Not ₹40 lakh. Not ₹20 lakh. Zero.

Interstate D2C sellers: One shipment across state lines triggers mandatory registration.

Multi-warehouse brands: Separate GSTIN per state. Separate filings per state. Budget ₹3,000-₹6,000/month per additional GSTIN for compliance costs. It is still cheaper than getting caught.

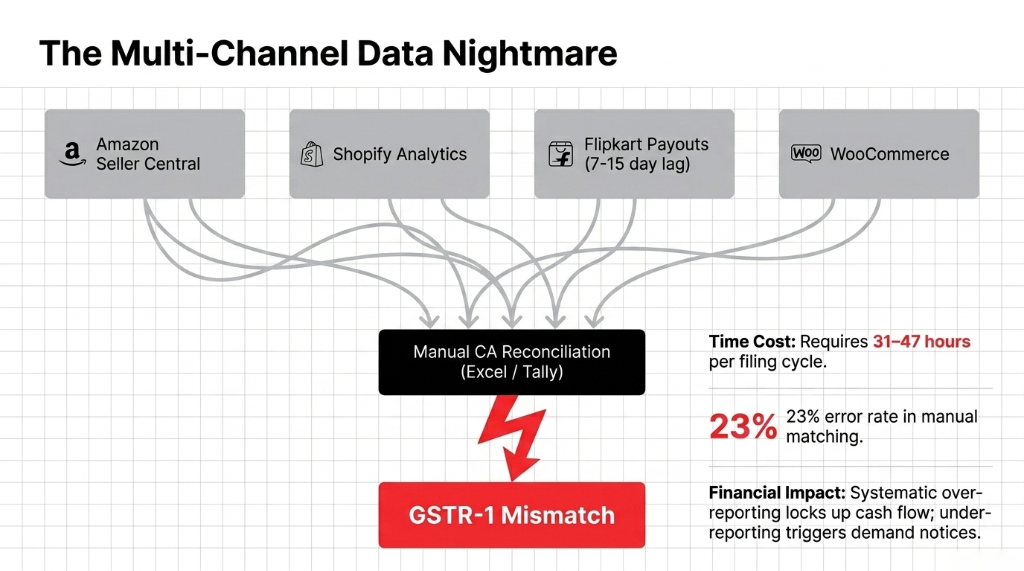

The Multi-Channel Reconciliation Nightmare

This is where most D2C brands quietly bleed out. Your Amazon sales go into Amazon Seller Central. Your Shopify sales go into Shopify Analytics. Your Flipkart payouts arrive 7-15 days after the actual sale. Your WooCommerce orders live in yet another database. And your accountant is trying to match all four data streams to your GSTR-1 every month — manually, in Tally or Excel.

The result? Systematic under-reporting or over-reporting of outward supplies in GSTR-1. Both are problems. Under-reporting triggers a demand notice. Over-reporting means you have over-paid tax and locked up cash flow unnecessarily. The process takes 31-47 hours per month. It costs ₹8,000-₹22,000 in CA fees per filing cycle. And it is still wrong 23% of the time because the human reconciling it does not catch returns, partial shipments, or B2B invoice discrepancies.

The TCS Money You Are Lending the Government at 0% Interest

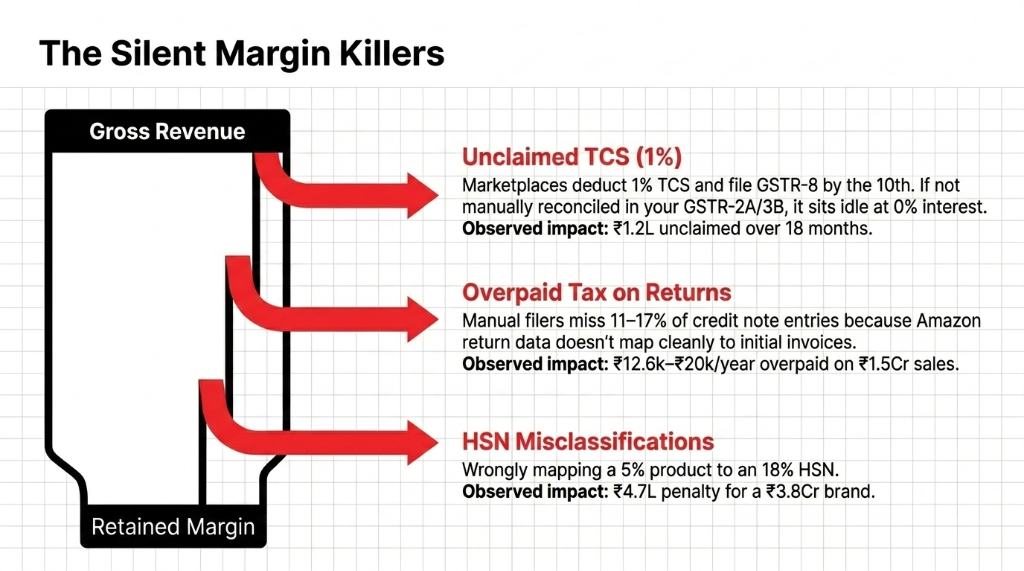

Here is what marketplaces do that most founders do not fully understand: Amazon and Flipkart deduct 1% TCS (Tax Collected at Source) on your net taxable sales before they pay you. On ₹50 lakh of annual marketplace sales, that is ₹50,000 sitting in your GST portal's cash ledger — money you have already "paid" but can only claim back by properly reflecting it in your returns.

We have worked with brands that had ₹1.2 lakh in unclaimed TCS credits sitting idle for 18 months because nobody reconciled their GSTR-2A. That is working capital you lent to the government at 0% interest. Your CA should have caught this. They did not.

The TCS math is not complicated. Each marketplace files a GSTR-8 by the 10th of every month, and the amount they collect appears in Part C of your GSTR-2A on the common portal. You claim it when filing your GSTR-3B. Simple in theory. Catastrophic in practice when you have four channels and a CA who is manually downloading four different settlement reports.

Why Your Accountant's "Manual Reconciliation" Will Kill Your Margins

We constantly see this mistake: founders hand over four separate sales reports — Shopify CSV, Amazon Settlement, Flipkart Payment Summary, WooCommerce export — and ask a CA or junior accountant to reconcile them into GST returns. The human doing this work does not catch returns, partial shipments, or marketplace fee adjustments that shift taxable value.

The HSN Code Problem Nobody Talks About

Misclassify your product's HSN code — say, put a 5% GST product under an 18% HSN — and two things happen. You overcharge your customers (which means refunds, complaints, and chargebacks). Or you under-remit tax to the government (which means demand notices with interest). Both outcomes have happened to our clients.

One of them, a ₹3.8 crore/year apparel brand, had ₹4.7 lakh in HSN misclassification penalties pending before they came to us. The fix took 3 weeks. The damage took 14 months to accumulate.

The B2B Invoice Trap That Kills Your Wholesale Channel

B2B customers — retailers buying wholesale through your D2C website — cannot claim ITC unless your invoice is perfectly structured: GSTIN, HSN code, tax breakup, invoice date, and place of supply. One wrong field and your customer's ITC claim fails. They come back to you. You lose the repeat order. This is how D2C brands quietly kill their wholesale channel without even realizing it.

The Returns and Cancellations Problem That Blocks Your ITC

Returns are where multi-channel GST compliance gets genuinely painful. When a customer returns a product through Amazon, Amazon issues a credit note against the original invoice. But the original invoice has already been reported in your GSTR-1. The credit note reduces your tax liability — but only if you issue it within the prescribed time and report it correctly.

Most brands using manual filing miss 11-17% of credit note entries because the return data from Amazon Seller Central does not map cleanly to the invoice data in their accounting software. The downstream effect: your GSTR-3B shows a higher output tax liability than your actual net sales. You pay more GST than you owe.

The Return Tax Leak Nobody Notices

On ₹1.5 crore in annual sales with a 9% return rate (standard for apparel):

Missed credit notes = overpaid GST of ₹12,600-₹20,000/year

That is cash you handed to the government and never asked for back.

The Interstate Warehouse Trap Nobody Warns You About

You opened a Bhiwandi warehouse to serve Mumbai faster. Good logistics decision. Catastrophic GST decision if you did not register it.

Every time goods move from your Surat dispatch hub to your Bhiwandi warehouse, that is a stock transfer between two GSTINs, and it requires a proper tax invoice plus an e-way bill for consignments above ₹50,000. It is not a sale, so no GST is paid, but it must be reported in GSTR-1 as an outward supply under "Stock Transfer to Branch." Fail to do this and you have an unexplained inventory discrepancy between two state filings — exactly the kind of anomaly that triggers a GST audit.

We have seen brands with three warehouse states running "informal" stock transfers for 14 months before an e-way bill audit caught it. The reconciliation cost — in CA fees, interest, and penalties — was ₹1.87 lakh. The savings from not registering in those states were approximately ₹0.

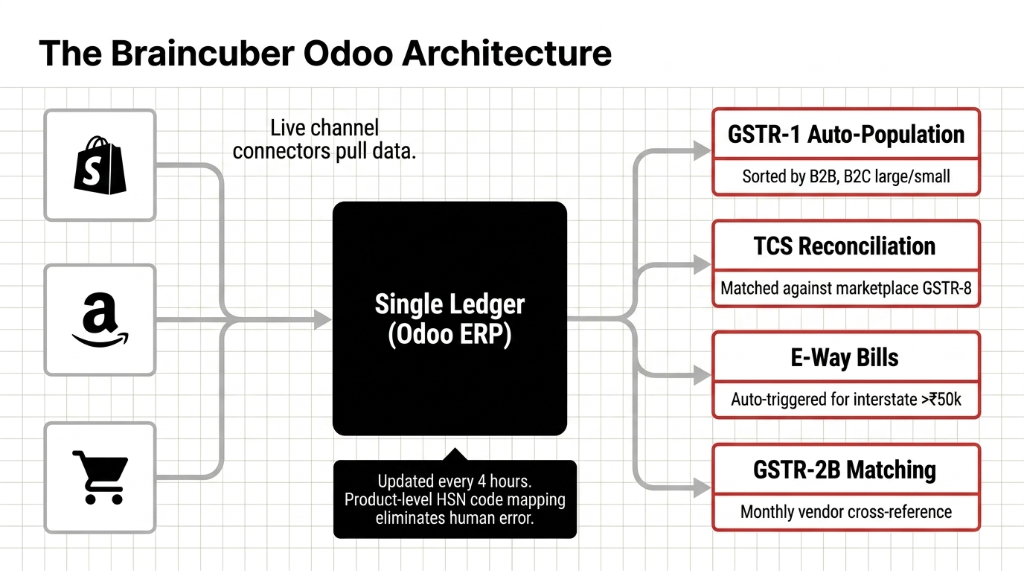

The Odoo Fix: How to Stop Filing on Faith

The Braincuber approach is not to "automate your existing mess." It is to rebuild the data flow from scratch. When we implement Odoo ERP for a D2C brand, here is the exact architecture:

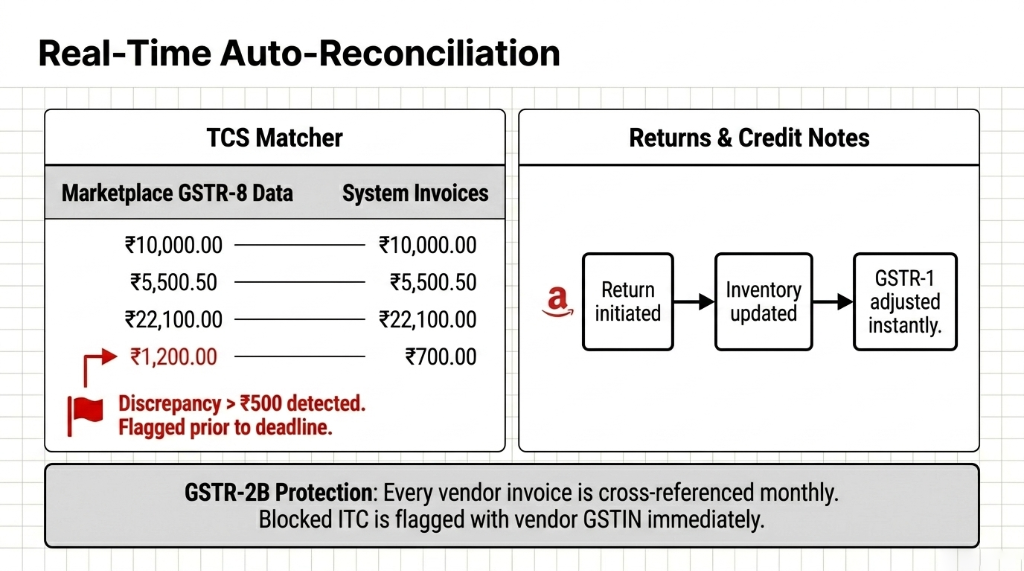

The Braincuber Odoo GST Architecture

Channel connectors pull live order data from Shopify, Amazon, and Flipkart into a single ledger — updated every 4 hours, not batch-processed at month-end.

HSN code mapping is done at the product level in Odoo, so every invoice generated across every channel uses the correct tax rate — no human decision point.

GSTR-1 auto-population pulls from Odoo's sales register directly, sorted by B2B, B2C large, and B2C small — exactly the format the GST portal expects.

TCS reconciliation happens automatically — Odoo matches marketplace GSTR-8 data against the invoices in the system and flags discrepancies above ₹500 before the filing deadline.

E-way bill generation is triggered automatically for any interstate order above ₹50,000, so your warehouse team never has to think about it.

GSTR-2B matching runs monthly: every vendor invoice in Odoo is cross-referenced against the GSTR-2B download, and any ITC that cannot be claimed is flagged with the vendor's GSTIN and outstanding amount.

Real Result: ₹2.1 Crore/Year D2C Personal Care Brand

Monthly GST filing time: Dropped from 41 hours to 6.5 hours.

TCS recovery: ₹83,000 recovered in the first 90 days.

First GSTR-9 annual return: Filed without a single revision notice. Their CA said it was the cleanest return they had seen in four years of practice. (Yes, their CA said that.)

What Annual GST Compliance Actually Costs a Multi-Channel D2C Brand

Let us be specific because this is where founders get surprised:

| Compliance Item | Manual/CA Model | Odoo-Automated Model |

|---|---|---|

| Monthly GSTR-1 + 3B filing (CA fees) | ₹4,000-₹12,000/month | ₹800-₹2,500/month |

| Annual GSTR-9 filing | ₹15,000-₹40,000 | ₹5,000-₹10,000 |

| Missed TCS recovery (avg, 3 channels) | ₹40,000-₹1.5L/year | ₹0 (auto-reconciled) |

| HSN misclassification penalties | ₹0-₹5L (risk-based) | Near-zero (system-enforced) |

| Man-hours on reconciliation | 31-47 hrs/month | 4-7 hrs/month |

A ₹4 crore/year D2C brand running manual compliance is spending ₹2.4-₹4.1 lakh annually on direct compliance costs, not counting the opportunity cost of founder time spent reviewing CA work. That same brand on Odoo with proper integrations spends ₹80,000-₹1.2 lakh and has a cleaner audit trail.

The Odoo Implementation Reality (No Sugarcoating)

Odoo GST setup for a 3-channel D2C brand takes 6-9 weeks from kickoff to first live filing. Not 2 weeks. Not "instant." Here is the real timeline:

The 9-Week Implementation Timeline

Week 1-2: Data Migration

HSN mapping at the product level. Historical data cleanup. SKU standardization across all channels. This is where 80% of implementations fail if rushed.

Week 3-6: Connectors + Parallel Run

Channel connector setup and testing. Parallel run with old system to catch discrepancies. Your CA verifies Odoo-generated returns against manual data one last time.

Week 7-9: Go-Live + First Filing

Live filing under the new system. CA training. Every Shopify order gets a GST-compliant invoice within 3 seconds — GSTIN, HSN code, tax breakup, digital signature. No more batch-generating invoices the night before filing.

The first month after go-live is the hardest — your CA will need to verify the Odoo-generated returns against manual data one last time. After that, the system runs without your daily intervention. What gets easier immediately, even in Week 1: invoice generation. That alone saves 11-17 hours per filing cycle for most brands we onboard.

5 Questions Every Multi-Channel D2C Founder Asks About GST

Do D2C brands need GST registration even if turnover is below ₹40 lakh?

Yes. If you sell on Amazon, Flipkart, Meesho, or any e-commerce marketplace, GST registration is mandatory from your first rupee of sales. Section 24(ix) of CGST Act removes the turnover threshold for marketplace sellers. Interstate sales from your own website also trigger mandatory registration regardless of turnover.

What is TCS under GST and how does it affect D2C payouts?

Marketplaces like Amazon and Flipkart deduct 1% TCS on your net taxable sales before paying you. They deposit it with the government and file a GSTR-8 by the 10th of the following month. You claim this back by matching it in your GSTR-3B. On ₹50 lakh in marketplace sales, that is ₹50,000 in TCS you must actively recover, or it sits idle in your cash ledger.

How many GST returns does a multi-channel D2C brand file monthly?

At minimum: GSTR-1 (outward supplies, due 11th) and GSTR-3B (summary return with ITC and liability, due 20th). Annually: GSTR-9. If you have multiple state GSTINs — say, warehouses in Gujarat and Maharashtra — you file separate GSTR-1 and GSTR-3B for each state every month. Three-state warehouse brands file 6+ returns monthly.

Can I claim ITC on packaging, warehousing, and logistics costs?

Yes, but only if your vendor is GST-registered, has uploaded the invoice on GSTN, and has paid the tax. If your packaging supplier is unregistered or a late filer, your ITC claim fails even if you have a valid invoice. Reconciling your GSTR-2B every month and following up with non-compliant vendors is the only way to protect your ITC.

What happens if I transfer stock between warehouses without documentation?

Each inter-state stock transfer requires a GST invoice and an e-way bill for consignments above ₹50,000. Undocumented transfers create inventory discrepancies between state filings, attract scrutiny during GST audits, and can result in demand notices treating the transfer as an unrecorded taxable supply — with interest at 18% per annum.

The Real Cost Is Not the Penalty. It Is the Cash You Never Recovered.

Every month you file GST manually across multiple channels, you are leaving TCS credits unclaimed, overpaying on returns you did not reconcile, and risking HSN penalties that compound silently. The brands that fix this early do not just avoid notices — they recover ₹83,000-₹1.5 lakh in the first 90 days. The brands that wait? They fund the government's cash ledger for free.

Open your GST portal right now. Check Part C of your GSTR-2A. If there is unclaimed TCS sitting there from 3+ months ago, you have a problem.

We identify the exact leakage in a 15-minute operations audit — TCS recovery, HSN misclassification, and multi-state filing gaps. Most brands we audit recover the cost of the fix in the first quarter.

Book Your Free 15-Minute GST Audit