If you are spending money on AI tools in Q3 and Q4 2026 without a coordinated tax strategy, you are not just overspending — you are donating directly to the IRS.

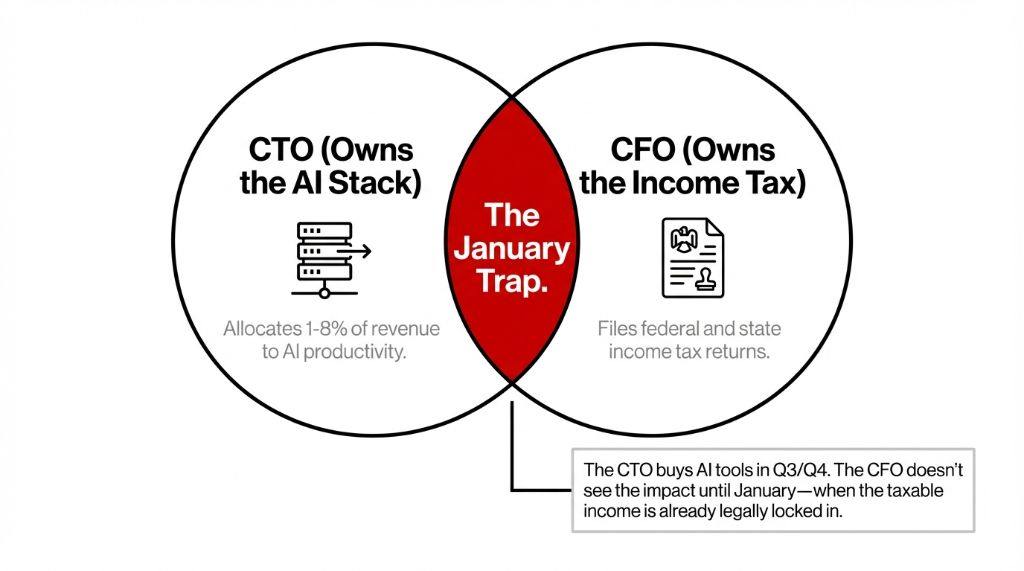

We know this because we have audited over 150 US businesses across New York, Texas, California, and Florida, and the same mistake shows up every time: the CFO owns the income tax filing, the CTO owns the AI stack, and the two never talk until January — when it is too late to do anything about the taxable income that already locked in.

This guide fixes that. By the end, you will know exactly how to structure your AI spend for H2 2026 in a way that legally reduces your business income tax, avoids the capital gains tax traps most companies stumble into, and puts every dollar of AI budget on the right side of the IRS classification system.

The H2 2026 AI Cost Picture Nobody Shows You

AI budgets are set to nearly double in 2026, with companies already allocating 1–8% of total revenue to AI productivity initiatives. For a $4M US business, that is between $40,000 and $320,000 a year in AI spend.

Here is the ugly truth about that number: how you classify it determines which tax bracket you end up in.

If you expense $120,000 in custom AI development as a current operating cost instead of a capital expenditure eligible for the federal R&D tax credit, you are over-reporting taxable income in Q3 and under-claiming the credit in Q4. At the 24% income tax bracket, that single misclassification costs you $11,760 in income tax you did not legally owe.

The IRS updated the 2026 tax bracket thresholds by roughly 2% for inflation. The seven federal income tax rates — 10%, 12%, 22%, 24%, 32%, 35%, and 37% — stayed exactly the same. What changed are the income tax thresholds tied to each rate.

| Rate | Single Filer | Married Filing Jointly |

|---|---|---|

| 10% | Up to $12,400 | Up to $24,800 |

| 12% | $12,401–$50,400 | $24,801–$100,800 |

| 22% | $50,401–$105,700 | $100,801–$211,400 |

| 24% | $105,701–$201,775 | $211,401–$403,550 |

| 32% | $201,776–$256,225 | $403,551–$512,450 |

| 35% | $256,226–$640,600 | $512,451–$768,700 |

| 37% | $640,601+ | $768,701+ |

The 2026 standard deduction is $16,100 for single filers and $32,200 for married filing jointly — up from $15,750 and $31,500 in 2025. These numbers matter for H2 planning because every dollar you reclassify correctly either keeps you in a lower tax bracket or pulls you back from crossing into a higher one unnecessarily.

Why "Just Expense Everything" Is a $23,000-a-Year Mistake

We constantly see clients doing this. Their accountant says "put it all under software." The QuickBooks chart of accounts gets one line called "AI & Tech Tools," and everything gets written off as an operating expense.

That works for a $19/month ChatGPT subscription. It does not work when you are talking about:

The Three AI Costs Your Accountant Keeps Mislabeling

1. A $45,000 custom AI agent built on LangChain or CrewAI

2. $28,000 in AWS SageMaker training costs for a proprietary demand forecasting model

3. $67,000 in Azure OpenAI deployments running production business logic

These are not SaaS subscriptions. They are capital investments — and misclassifying them destroys two things: your real income tax rates exposure for H2, and your eligibility for the federal R&D tax credit under IRC §41.

That credit is dollar-for-dollar against taxes owed. Not a deduction that reduces your taxable income. A direct offset against your actual income tax bill.

The Big Tech Proof

Amazon dropped their corporate income tax bill from $9 billion in 2024 to approximately $1.9 billion in 2025 using AI R&D credits, infrastructure depreciation, and federal tax deductions on capital investments. Meta went from $9.6 billion to $2.8 billion using the same playbook.

You do not need to be Amazon

Any US company that builds, trains, or meaningfully customizes AI tools — including a $2.5M D2C brand building a recommendation engine in Shopify — qualifies.

Difference at $3M revenue, 24% bracket: ~$23,000/year

The Capital Gains Tax Trap Sitting Inside Your AI Budget

This is the one your accountant is probably not flagging.

If your AI stack includes automated investment tools, AI-driven equity strategies, robo-advisory modules, automated FX hedges, or dividend-generating AI portfolios, you have a capital gains taxation event sitting inside your tech budget — and the capital gains tax rate 2026 differentials are enormous.

The Capital Gains Gap: 17 Points at the Top End

Short-Term (Under 12 Months)

Taxed at your ordinary income tax rates — up to 37% federally. Every AI-generated trade you close before the 12-month mark gets treated as regular income.

Long-Term (12+ Months)

The long-term capital gains tax rate sits at 0%, 15%, or 20% depending on your income tax bracket. For most US companies in the 22–24% bracket, the federally applied rate is 15%.

The Math on an $82,000 AI-Generated Return

Short-term at 37%: $30,340 in tax. Long-term at 20%: $16,400 in tax. Difference: $13,940 in unnecessary federal tax. That is not optimization. That is just reading the rules before you close a position.

California Warning

State income tax treatment in California taxes long-term capital gains as ordinary income at the state level — up to 13.3%. The federal long-term advantage disappears entirely at the state level. Your capital gains tax picture is always federal plus state. Never just federal.

The Payroll Tax Reality When AI Replaces Headcount

When your company replaces a $71,000/year operations manager with an AI agent, the payroll taxation math changes instantly.

The combined social security payroll tax rate — employer plus employee — is 15.3% (12.4% Social Security + 2.9% Medicare). On a $71,000 salary base, that is $10,863/year in payroll tax the company was funding. Automating that role saves you the salary and the payroll tax contribution.

But the Math Punches Back

The problem: That $71,000 salary was a deductible operating expense reducing your taxable income. Remove it and replace it with an $18,000/year AI tool subscription, and your taxable income increases by $53,000.

At the 24% business income tax rate

That adds $12,720 to your federal income tax obligation before you count state income tax on top.

Net surprise: $12,720 in higher income tax

The Dallas Logistics Case

We worked with a $5.3M logistics brand in Dallas that replaced three operations staff with custom agentic AI workflows. Their payroll tax savings were $31,824 in year one. Their CFO did not remodel the resulting income tax bracket exposure shift.

What happened next

They underpaid Q3 and Q4 estimated taxes by $11,300 and received a $1,740 IRS underpayment penalty. Their net first-year AI saving dropped from $53,000 to $39,960 because of a 45-minute planning conversation they skipped.

Also: if your AI engineers are misclassified as 1099 contractors when they should be W-2 employees, the IRS can hit you with back employee tax obligations, social security tax rate liabilities, and interest that runs 3–5x the original salary savings.

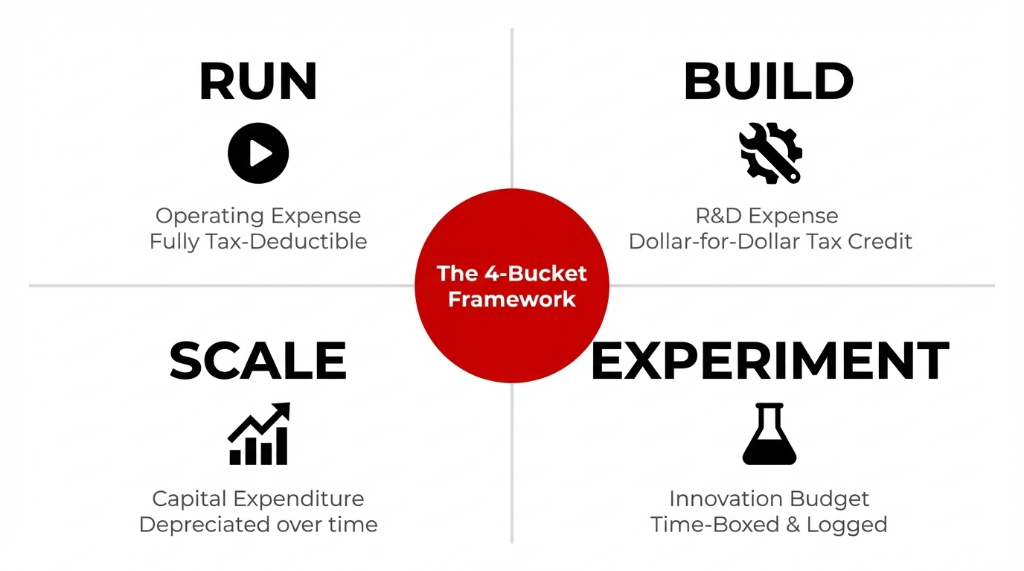

How to Structure Your H2 2026 AI Budget — Four Buckets, No Exceptions

This is the classification framework we use for every client before Q3 locks in.

The 4-Bucket AI Budget Framework

Bucket 1: Run (OpEx, Fully Deductible)

Monthly SaaS AI tools under $5,000/month: ChatGPT Enterprise, Anthropic API, Jasper, Midjourney. Operating expenses under IRC §162. Deduct them fully in the year paid. The closest thing to tax-free AI spend you will find.

Bucket 2: Build (R&D, Tax Credit)

Custom AI agent development, LangChain/CrewAI pipelines, proprietary ML model training, Document AI builds. These qualify for the federal R&D tax credit — a direct reduction in your actual income tax bill. Every dollar your accountant mislabels as "software expense" here is a dollar you overpaid.

Bucket 3: Scale (CapEx, Depreciated)

GPU clusters, dedicated AWS/Azure/GCP AI infrastructure, large-scale SageMaker model training runs. Capital expenditures depreciated under MACRS — not current-year expenses. Treating them as OpEx either over-states your H2 deductions (audit flag) or under-states your long-term tax reduction spread.

Bucket 4: Experiment (Innovation, Time-Boxed)

Pilot programs, vendor trials, proof-of-concepts under $8,000. Typically expensed directly in the year incurred. Keep detailed time logs and business purpose documentation — the IRS will ask during any exam of your business tax classification.

The H2 2026 Month-by-Month Action Plan

April–May 2026 (Revisit Now If You Skipped It)

Audit every H1 AI expense. Reclassify against the four buckets. Run a 2026 tax bracket income scenario model using your H1 actuals projected forward. If you are within $30,000 of the next income tax thresholds boundary, this is the moment to decide whether to accelerate or defer AI capital expenditures.

June–July 2026

Lock in R&D credit documentation for every custom AI build in flight. Collect time logs, technical experiment records, and project scope documents — these are the evidence the IRS requires. Also decide whether AI-generated investment positions need to be held past the 12-month mark to convert short-term capital gains into long-term capital gains. That decision has to be made in June for assets acquired in Q2 2025.

August–September 2026

Review dividend taxable income from any AI-driven investment holdings. Qualified dividends receive the same preferential tax rates as long-term capital gains (0%, 15%, or 20%). Non-qualified dividends hit at ordinary US income tax rates — up to 37%. Check whether your dividends qualify before Q4.

October–November 2026

Finalize year-end tax planning moves. Time AI software renewals against your income tax scale — renewing in December captures the deduction in 2026; renewing in January shifts it to 2027 taxable income. Run the short-term capital gains calculator on every position you plan to close before December 31. Long-term capital gains taxation treatment requires a 12-month hold — if a position hits that mark in October, waiting 6 weeks to close could save $9,000–$19,000 in capital gains tax.

December 2026

Do not close AI-generated investment positions based solely on the federal capital gains rate without checking your state's overlay. States like California and New York treat long-term capital gains as ordinary state income — meaning the capital gains tax bracket savings at the federal level disappear at the state level. Your true tax rate is always federal plus state combined.

The "Tax-Free" AI Strategies That Actually Exist

Some AI investment income can legitimately grow with no short-term capital gains or long-term capital gains exposure annually — and it is not a loophole.

Roth IRA, Roth 401(k), and HSA Structures

If founders or executives run AI-driven investment strategies inside a Roth IRA, Roth 401(k), or HSA, returns compound without triggering annual capital gains taxation or income tax events. The income-tax-free compounding inside a Roth structure is particularly powerful for AI portfolios that generate frequent short-term trading activity — because each trade inside the account does not create a taxable event.

This is not universal advice. Contribution income thresholds and business structure requirements apply. But if you are a US founder earning above the direct Roth contribution thresholds, there are clean workarounds. The point: tax-free treatment on AI returns is not theoretical — it is in the tax code right now, and most founders never touch it. *(Yes, your accountant will hate this.)*

FAQs

Are AI software subscriptions fully tax-deductible as business expenses in 2026?

Yes. SaaS AI tools like ChatGPT Enterprise or Jasper are operating expenses under IRC §162, fully deductible against business income tax in the year paid. Custom AI development costs qualify separately for the federal R&D tax credit — a dollar-for-dollar reduction in income tax owed, worth an average of $14,200/year for a $3M company.

How does replacing employees with AI affect my payroll tax obligations?

Every W-2 employee replaced with AI reduces your employer payroll tax liability by 7.65% of that salary. On a $68,000 role, that saves $5,202/year. But the salary was a deductible expense, so your taxable income rises by the difference between the old salary and the new AI tool cost. Always remodel your income tax bracket exposure first.

What is the capital gains tax rate on AI-generated investment returns in H2 2026?

Federally, long-term capital gains on positions held 12+ months stay at 0%, 15%, or 20%. Short-term capital gains are taxed at ordinary federal income tax rates up to 37%. Run a capital gains calculator before closing any AI-generated position in Q3 or Q4.

Can we claim the federal R&D tax credit for AI development work in H2 2026?

Yes, if the work meets the IRS four-part test: improved functionality, technical uncertainty, process of experimentation, and technological nature. Custom agentic AI builds, LangChain pipelines, and proprietary ML training typically qualify. Unlike a standard deduction, the R&D credit reduces actual income tax owed dollar-for-dollar.

Does the 2026 standard deduction change how I structure AI business expenses?

The 2026 standard deduction ($16,100 single / $32,200 married filing jointly) applies to personal returns only. For LLCs, S-Corps, and C-Corps, all qualifying AI expenses are itemized directly against business income tax. Sole proprietors must compare the standard deduction against actual itemized deductions to find the lower tax outcome.

Pull Up Your QuickBooks Right Now. Find "AI & Tech Tools."

If every AI dollar you spent in H1 is sitting under one line item, you are already bleeding cash on your H2 tax bill. We will run a 15-minute audit of your AI classification, remodel your income tax bracket exposure against the four-bucket framework, and hand you the exact dollar amount your current setup is costing you before December 31. No charge. No pitch deck. Just the number.